What Orlando Homeowners Need to Know About 4 Point Inspections

Florida's insurance crisis turned a routine underwriting tool into a gatekeeper for coverage. Here's what inspectors examine, which findings kill applications, and what it costs locally.

What Orlando Homeowners Need to Know About 4 Point Inspections

Florida’s insurance crisis turned a routine underwriting tool into a gatekeeper for coverage. Here’s what inspectors examine, which findings kill applications, and what it costs locally.

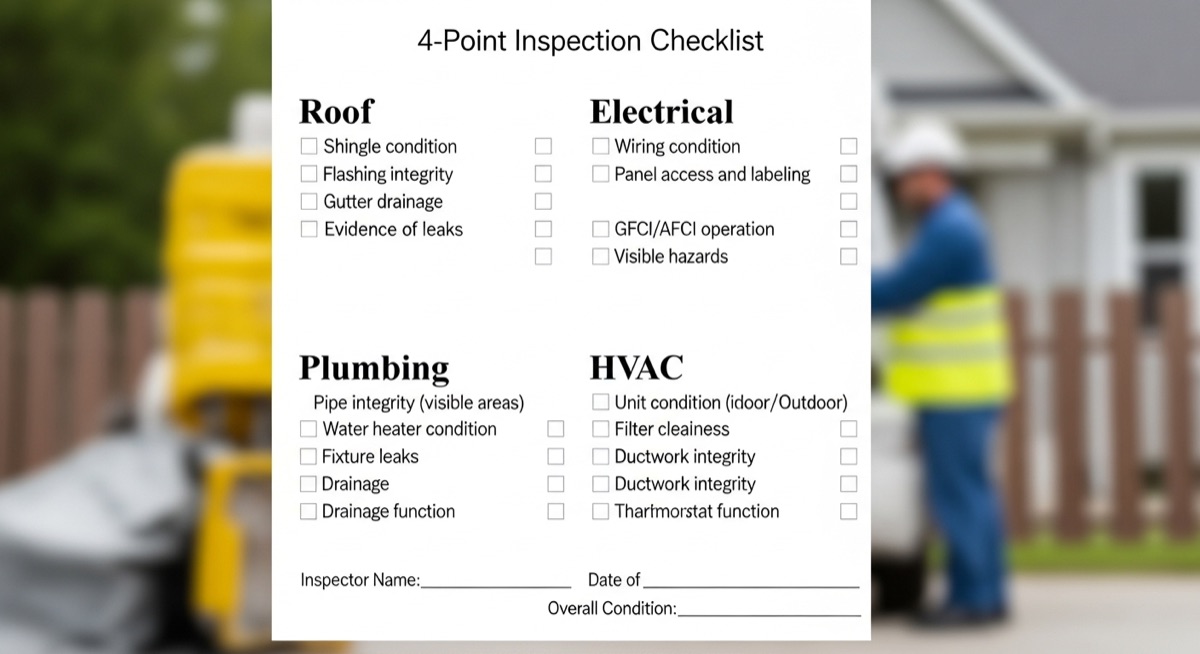

A 4-point inspection covers four systems: the roof, electrical panel and wiring, plumbing, and HVAC. Florida insurance carriers require it because those four systems generate the majority of claim exposure in older homes. Documented on a standardized state form, it’s become essential to underwriting. If any system is past useful life or contains materials carriers consider uninsurable, the application stalls — or dies. In Central Florida’s aging housing stock, that outcome is increasingly common.

Why This Inspection Suddenly Matters More Than It Used to

Five years ago, a 4-point inspection was something your parents dealt with when they bought a house in the ’80s. Today it’s routine across some of Orlando’s most established neighborhoods — College Park, Azalea Park, MetroWest, Conway. The reason is straightforward: Florida’s private insurance market collapsed around them.

The legislature responded with SB 2-A in late 2022 and HB 837 in 2023, reforms designed to curb litigation costs and stabilize the market. Those bills bought time, but they didn’t reverse the underwriting tightening that insurers had already set in motion. Carriers that stayed in Florida are writing fewer risks and scrutinizing the ones they write more carefully than at any point in recent memory.

For Orlando homeowners, this means something concrete. Many private carriers that once drew the line at 30-year-old homes moved their threshold to 20 years — and some to 15. Orlando’s core neighborhoods were largely built between 1950 and 1995. The suburban rings of the 1980s and early 1990s are now well inside that window.

This puts tens of thousands of local homeowners in an unexpected position: learning, often for the first time at renewal or when shopping for a new policy, that they need an inspection they’d never heard of. It’s a frustrating way to find out, and it’s avoidable.

The Four Systems — What Inspectors Actually Evaluate

The inspection is formally documented on Florida form OIR-B1-1802, issued by the state’s Office of Insurance Regulation. A general home inspection report — the kind a buyer gets at closing — does not satisfy this requirement, even if it’s thorough and recent. Insurers check for the 4-point form by name. Don’t assume your closing paperwork covers this.

Only certain licensed professionals may sign the form: licensed home inspectors, general contractors, building contractors, engineers, and architects. A handyman’s assessment or a contractor’s written opinion doesn’t meet the standard.

Roof. The inspector documents roofing material, approximate installation date, overall condition, and estimated remaining useful life. They examine granule loss on shingles, cracking or lifting on tile, evidence of patching, and whether there’s any documentation of prior replacement. Permits matter here — an unpermitted re-roof might look fine from the street but creates problems discussed below.

Electrical. This section covers the panel brand, wiring type — aluminum branch circuit, knob-and-tube, or standard copper — and service amperage. The inspector notes whether the panel has known safety defects. For Federal Pacific and Zinsco panels, that question is essentially settled before they open the box. They’re also looking for signs of DIY wiring and whether the amperage meets current standards.

Plumbing. The inspector identifies visible supply line material — copper, CPVC, PVC, or polybutylene — and the age and condition of the water heater. They note active leaks and whether the water heater has a properly installed pressure relief valve. Shorter section than electrical, but the findings can be just as consequential.

HVAC. Age and condition of the air handler and condenser, refrigerant type, general functional status. The inspector isn’t doing a mechanical evaluation the way an HVAC technician would. They’re confirming the system exists, how old it is, and whether it appears to be running. For R-22 systems — older refrigerant banned from production under the EPA’s January 2020 rule — the age implication is automatic.

How Old Is “Old Enough” — and Why the Answer Varies by Insurer

The figure you’ll hear most often is 30 years. It’s outdated.

Citizens Property Insurance Corporation currently requires a 4-point for homes 25 years or older at application or renewal. Private carriers are drawing the line earlier. Universal Property & Casualty, Heritage, Tower Hill, and most others active in Central Florida now require it at 20 years, and several have moved to 15. If your home was built in 2005 or earlier, you may already be inside at least one carrier’s trigger window. If it was built in the 1980s or 1990s — the case for much of MetroWest and Pine Hills — you’re inside all of them.

Every carrier sets its own threshold, and those thresholds shift with the underwriting environment. Homeowners shopping after a non-renewal should ask the specific carrier what age triggers the requirement, and whether that threshold applies at renewal as well as initial application. Several carriers now require updated inspections at renewal even when an existing report is on file. That one surprises people.

The Orlando-Specific Red Flags

Some findings on a 4-point are negotiable. Others end the conversation.

Federal Pacific Stab-Lok and Zinsco panels. If your home was built between roughly 1950 and 1990, there’s a real chance the electrical panel is one of these. FPE Stab-Lok panels were common across Florida from the 1950s through the mid-1980s; Zinsco ran through roughly the same era. Both have documented histories of breakers that fail to trip under overload, and both are near-automatic declines at Citizens and virtually every private carrier writing in Florida. Inspectors recognize them on sight. A licensed electrician can confirm the brand in five minutes — it’s usually printed on the panel door. Worth checking before you pay for a report.

Polybutylene pipe. The gray flexible plastic supply line installed across Florida from about 1978 through 1995 was the subject of a national class-action settlement after widespread failures. MetroWest, parts of Pine Hills, older Kissimmee corridors — all were built heavily with poly-B, as was much of the mid-1980s construction across Orange and Osceola counties. Citizens treats active polybutylene as a hard decline. Most private carriers follow the same rule.

Knob-and-tube wiring. Less common in post-WWII construction, but still present in Colonialtown, Delaney Park, and other neighborhoods built before about 1950. Knob-and-tube is ungrounded, can’t be insulated without overheating risk, and no carrier in the current market will touch it. If a home still has active knob-and-tube, it isn’t insurable until the wiring is replaced.

Roofs approaching or past 30 years. No major Florida carrier will write a home with a roof at or past 30 years, regardless of how the shingles look. Some have tightened to 25, or 20 for certain materials. The reasoning is actuarial: a roof that old is likely to fail within the policy term. And Orlando’s combination of intense UV, high humidity, and hurricane exposure stresses shingles harder than the same roof would face in Georgia or the Carolinas. A 28-year-old shingle roof here has earned every year of that age. For more on preparing your home’s exterior against storm damage, see our coverage of how to harden your Orlando home before hurricane season.

Unpermitted roof replacements. If a prior owner replaced the roof without pulling a permit from Orange County Building Division — common in the 2000s and early 2010s — the inspector may flag it, and it will likely surface in a permit search. An undocumented re-roof creates two problems simultaneously: the insurer can’t confirm installation date or quality, and the gap complicates any future sale. Orange County’s permit records are searchable at ocfl.net/Growth/BuildingDivision.aspx. Check before you schedule the inspection. Five minutes of searching beats a last-minute scramble.

Why Florida’s Climate Makes These Systems Age Faster

A residential HVAC system nationally averages 15 to 20 years of useful life. In Orlando, running year-round under full cooling demand, 12 to 15 is more realistic. A 15-year-old air handler in Orlando has been running without an off-season since installation. A comparable unit in a northern climate has been switched off for six months of every year. The mechanical wear isn’t even close.

Humidity compounds the problem for roofs. High summer dew points, daily afternoon thunderstorms, and intense UV accelerate granule loss on asphalt shingles and promote algae growth that degrades surface integrity faster than in dry or cooler climates. An inspector noting an R-22 system is noting a system overdue for replacement — and one that’s increasingly expensive to service as remaining refrigerant supplies contract.

If you want to self-assess before calling an inspector: pull the data plate off your condenser and write down the manufacture date. Do the same for your water heater. Look at your electrical panel. If the brand reads “Federal Pacific,” “Stab-Lok,” or “Zinsco,” stop there and call an electrician before you call an inspector. You’ll want to understand your options before the report is generated and on the record.

What Happens When Your Home Fails — The Full Decision Tree

The vague language common in our home & property coverage — “the insurer may decline coverage” — understates the actual range of outcomes.

Hard decline. Certain findings trigger automatic rejection: an active FPE Stab-Lok or Zinsco panel, active polybutylene supply lines, active knob-and-tube wiring, or a roof with no remaining useful life. Application denied.

Conditional approval with exclusions. Some carriers will issue a policy but explicitly exclude the flagged system. A homeowner with aging plumbing might receive coverage that excludes water damage claims originating from plumbing failure. That’s not nothing — but it’s also not full coverage. Read every exclusion before you sign, because a policy that won’t pay your most likely claim is barely worth the premium.

Repair-and-resubmit. When a finding is serious but not an automatic hard stop — a deteriorated roof with some remaining life, an older HVAC unit that’s functional but marginal — some carriers will issue a conditional offer. Complete the specified repair within a defined window, typically 30 to 90 days, provide documentation, and the application gets reconsidered. A licensed contractor’s letter describing in-progress work can sometimes hold the window open. What counts as adequate documentation varies by carrier; a local independent agent who works with multiple insurers will know what a specific company will actually accept.

Citizens as last resort. If private carriers decline, Citizens is legally required to offer coverage to Florida property owners who can’t obtain it elsewhere — subject to its own underwriting standards, which are real. Citizens will also decline for hard-stop findings like active poly-B or FPE panels. But for borderline cases where private carriers are simply unwilling to write the risk, Citizens is the fallback. Get a local independent agent here, not a direct-to-consumer website. The nuances matter too much.

One practical note: some findings that look like hard stops have a resolution path if the homeowner moves quickly. An electrician’s signed letter confirming a panel replacement is contracted and permitted can sometimes keep an application alive through a short window. This varies by carrier and finding. But it’s worth knowing before you assume the door is closed.

What It Costs in Orlando

A standalone 4-point inspection from a licensed inspector in Orange, Seminole, or Osceola County typically runs $75 to $150, depending on home size and inspector.

A bundled 4-point plus wind mitigation report — both completed in one site visit — typically runs $150 to $250 in the same market. The wind mitigation report documents features that can reduce your premium: hip roof geometry, roof deck attachment method, opening protection, roof-to-wall connection type. For any home already in the trigger age window, the extra $50 or $75 to bundle both reports is an easy call. If you’re already paying for one, pay for the other.

How to Find a Qualified Inspector and What to Ask Before You Book

Florida statute is specific: the person signing the OIR-B1-1802 must be a licensed Florida home inspector, general contractor, building contractor, engineer, or architect. An HVAC technician, handyman, or roofer cannot legally sign the form. Confirm this before you book.

Two directories with Florida-specific search tools: InterNACHI at internachi.org and ASHI at homeinspector.org both let you filter by location.

Ask three questions before you commit:

Do you have experience with the specific issues in Central Florida’s older housing stock? You want someone who recognizes an FPE Stab-Lok panel on sight, knows what polybutylene looks like, and understands what local carriers are looking for. Any experienced inspector in this market should answer that confidently and specifically.

How quickly can you deliver the completed, carrier-ready report? If you’re on a renewal deadline, “a few days” isn’t good enough. Pin down an actual date.

Do you complete wind mitigation reports simultaneously? If yes, get the bundled price. If no, ask for a referral or find a different inspector.

Most Florida carriers accept 4-point reports up to three years old; some private carriers accept up to five. Don’t assume. Confirm current standards directly with your carrier before your renewal date — that assumption has cost more than a few homeowners I’ve heard from a scramble they didn’t need.

Quick-Reference: Pass/Fail Signals by System

Common findings summarized. Thresholds vary by carrier — confirm with a licensed independent agent before drawing conclusions.

| System | Typical Pass Conditions | Hard-Stop or High-Risk Findings |

|---|---|---|

| Roof | Shingle or tile under 20 years; documented replacement with permit; rated useful life remaining | Any material at or past 25–30 years; no remaining useful life; unpermitted replacement; active leaks or significant damage |

| Electrical | Standard copper wiring; 150- or 200-amp service; no defective panel brands | Federal Pacific Stab-Lok or Zinsco (near-automatic decline); active knob-and-tube; aluminum branch circuit wiring; 60-amp service |

| Plumbing | Copper or CPVC supply lines; water heater under 15 years with functioning PRV | Active polybutylene (Citizens hard decline; most private carriers decline); water heater over 15 years or lacking PRV; active leaks |

| HVAC | System under 12–15 years; R-410A refrigerant; functional | System 15+ years; R-22 refrigerant; non-functional or absent |

The 4-point inspection isn’t a bureaucratic inconvenience. It’s an assessment of the four systems that generate the most insurance losses in residential property — and in a state where carriers are scrutinizing every application, it increasingly determines whether coverage exists at all. For Orlando homeowners in houses built before 2000, knowing what inspectors are looking for before the report is generated is the difference between managing the outcome and being blindsided by it. The surprise is almost always the more expensive option.