How Much Can a Wind Mitigation Inspection Save on Your Orlando Insurance

Eight items. One form. Potentially $1,000 off your annual premium — if your home qualifies.

How Much Can a Wind Mitigation Inspection Save on Your Orlando Insurance

Eight items. One form. Potentially $1,000 off your annual premium — if your home qualifies.

A wind mitigation inspection is one of the few things an Orlando homeowner can do right now that has a real chance of putting several hundred to over a thousand dollars back in their pocket annually. Not eventually. At the next renewal cycle. The inspection produces a completed state form, which you hand to your insurer, and your insurer then uses it to recalculate the wind portion of your premium based on what your house is actually built to withstand.

Here’s what the process involves, what inspectors are physically looking for, and what you can realistically expect it to cost and save in Orange County.

Why Orlando Homeowners Underestimate This

Wind mitigation is not a coastal concern — not something reserved for people in Brevard County or along the Gulf. Orange County sits roughly 60 miles inland from either coast, but that distance has not historically kept storm energy from arriving with consequence.

Hurricane Charley crossed the peninsula in 2004 and caused significant wind damage in metro Orlando. Hurricane Ian made a nearly identical track in September 2022 and, though it had weakened from Gulf Coast landfall, still produced damaging gusts throughout the area. It also triggered the wave of roof replacements in 2022 and 2023 that continues to push local insurance pricing higher. If you’ve been watching your premium climb since then, that’s part of why.

The Florida Building Code designates most of Orange County in the 110–120 mph wind speed zone. That’s high enough that insurers use it as the basis for real surcharges — and real credits when a home demonstrates resistance to those speeds.

The houses with the most to gain from a wind mitigation inspection tend to be older. Pre-2002 construction predates the post-Andrew overhaul of Florida’s building code. That description covers large portions of Winter Park, Pine Hills, Conway, and Azalea Park, neighborhoods where housing stock from the 1960s through the 1990s is common and where an inspection can surface genuine credit opportunities — or at least clarify which upgrades would actually be worth the money.

Newer developments in Lake Nona and Horizon West, where construction largely postdates 2002, often arrive with multiple credits already built in. But getting the inspection done and having the OIR-B1-1802 form on file is still required if you want those credits applied. They are not automatic. Your insurer will not credit you for features it has not verified. It won’t just take your word for it.

What the Inspection Actually Is — and Who Can Legally Do It

A Florida wind mitigation inspection is not a general evaluation or a subjective opinion. It’s the completion of one specific, state-standardized form: the OIR-B1-1802, published by the Florida Office of Insurance Regulation. That form, and only that form, is what your insurer will accept. Inspectors who arrive with proprietary templates or custom reports are not producing a document your insurance company is required to honor. Ask directly before hiring anyone what form they use.

The credential requirement is specific. The inspector must hold one of the following: a Florida-licensed home inspector certification, a general contractor license, an architect license, or a professional engineering license. A mold assessor, a roofing salesperson, or a handyman with a clipboard does not qualify.

When you call to schedule, ask for their license number and license type. Any legitimate inspector will give it without hesitation. You can verify it at myfloridalicense.com. For finding qualified inspectors who serve Orange County ZIP codes, NACHI.org maintains a searchable directory by location with credential information. Local referrals from your insurance agent often lead to inspectors who understand the documentation preferences of your specific insurer, which matters more than it sounds.

The Eight Items on the Form

The OIR-B1-1802 has eight rated elements. Each one affects your premium independently. Understanding what the inspector is physically assessing helps you anticipate what your report will say — and avoid surprises.

Building Code Compliance. The inspector notes whether your home was built or substantially re-roofed under the Florida Building Code (2001 or later), the South Florida Building Code, or an earlier standard. Homes built or reroofed after March 1, 2002 under the current FBC get a favorable designation here. This is foundational — it shapes how the rest of the form is interpreted.

Roof Covering. The inspector documents your roofing material — asphalt shingles, metal, tile, or other — and whether it carries a Miami-Dade Product Approval or Florida Product Approval rating. A rated covering earns a credit. An unknown or unrated material does not.

Roof Deck Attachment. This is one of the more physically involved parts. The inspector goes into the attic and examines the nails connecting the roof deck — typically OSB or plywood panels — to the rafters or trusses. Nail type, diameter, spacing. Eight-penny nails at 6-inch spacing or tighter is what the Florida Building Code required post-2002 and what earns the best credit. Older homes frequently show 6d nails at wider spacing, which earns little or nothing. The inspector measures and counts. This is not an estimate.

Roof-to-Wall Connection. Back in the attic, at each rafter or truss end, the inspector examines how the roof structure attaches to the exterior walls. There’s a hierarchy: toenails (weakest), single wraps, double wraps, and structural connectors. Double wraps or structural connectors — metal strapping that wraps fully around the rafter and attaches on both sides of the wall framing — earn the strongest credits. Many pre-mid-1990s Orlando homes show toenail connections only, which earn no credit and can actually increase the calculated risk.

Roof Shape. Hip (all sides slope to the exterior walls), flat, gable (two sloping sides with vertical triangular ends), or some combination. Hip roof geometry performs significantly better in high winds than gable. A qualifying hip roof can reduce the wind portion of your premium by 25 to 32 percent on its own — which is worth sitting with for a moment. A “complex hip,” where at least 90 percent of the roof area is hip-shaped, qualifies for the full credit. A primarily gable-ended home, even with small hip elements, does not.

Opening Protection. Every opening in the building envelope must be evaluated: every window, exterior door, garage door, skylight. The inspector documents whether each opening has rated protection — impact-rated glazing, Miami-Dade or Florida Product Approved storm shutters, or impact-rated doors and garage doors. Three tiers: no protection, partial protection, and 100% protection of all openings with rated products. “Partial” means what it says. One unprotected window in a home where everything else is impact-rated means you don’t qualify for the top tier. I mention this because it’s a surprisingly common situation — impact windows on the front of the house, original unprotected door on the back laundry room. That’s not 100%.

Secondary Water Resistance. Self-adhering modified bitumen underlayment — “peel-and-stick” — applied directly to the roof deck before the final roofing material goes on. Its purpose is to prevent water intrusion if the outer roof covering is damaged. SWR earns a credit. Homes reroofed before roughly 2007, or with standard felt underlayment only, typically don’t qualify unless it was specifically upgraded.

Roof Geometry. Some form versions treat this separately from general shape — specifically the hip percentage calculation. The inspector measures or estimates the proportion of the roofline that qualifies as hip. At 90 percent or more, you get the full credit. Below that, the credit diminishes or disappears depending on the insurer’s rate filing.

On every item, an “unknown” or “unable to verify” answer is treated by most insurers as the worst-case assumption. If the inspector can’t see nail spacing because the attic is packed with blown insulation and there’s no permit documentation, the form says “unknown” and you don’t get that credit. That’s not the inspector’s failure — it’s what the form requires. Pull whatever permits you have before the appointment.

The Features That Earn the Biggest Discounts

Hip roof shape produces the largest single credit available for most Orlando homes. This is a construction fact — you can’t convert a gable roof to a hip without rebuilding the roof structure. If you already have one, the credit is waiting to be captured. It just needs to be documented.

Full opening protection — every window, door, garage door, and skylight rated for impact or protected by rated shutters — can add another 15 to 45 percent reduction on the wind component, depending on the insurer’s rate filing. This is also the item most amenable to homeowner action. An older home with aluminum single-pane windows and no shutters has a clear path: replace with impact-rated units or install rated shutters on every opening. The upfront cost is real. In a market where wind insurance is a meaningful share of a typical annual premium, the payback period is worth calculating with your insurer before committing — but the math often works. For a broader look at how to harden your Orlando home before hurricane season, the tradeoffs between shutters, impact glass, and structural upgrades are worth understanding together.

Double-wrap or structural roof-to-wall connectors are cheapest to capture during a reroof, because the installation opens up attic framing and adding hurricane straps at that point costs relatively little in additional labor. If you’re reroofing anyway — and a lot of Central Florida homeowners have been since Ian — asking your contractor to install double-wrap straps and documenting it for the inspector means you can often achieve this credit for modest additional spend.

FBC-compliant roof deck attachment is similarly easiest to achieve at reroof, either through supplemental nailing of existing decking or full deck replacement. Either approach, documented with the permit, allows the inspector to credit the upgrade.

Secondary water resistance underlayment became standard practice in Central Florida roofing after the FBC updates, so homes reroofed in the last decade or so typically qualify. Ask your roofer what underlayment was installed and pull the permit to confirm, because the inspector will ask.

What Orlando Homeowners Can Realistically Save

Florida Office of Insurance Regulation data and Citizens actuarial studies on wind credits provide useful benchmarks, though the exact impact on any given policy depends on your insurer’s rate filing and how your home scores across all eight items.

For a home in the 110 mph wind speed zone, a hip roof alone can reduce the wind portion of the premium by 25 to 32 percent. Stack in full opening protection, compliant deck attachment, double-wrap connectors, and secondary water resistance, and the cumulative credits can be substantial.

On a $3,500 annual premium — a figure cited in Florida actuarial studies as typical for an older Orange County home — combined credits for a well-built house could realistically reach $800 to $1,400 per year. That makes the inspection one of the higher-return expenditures available to a homeowner in this market. As we’ve covered in our home & property coverage, insurance costs have become one of the defining variables in what Orlando homeownership actually costs right now.

For older homes in Conway, Pine Hills, or Azalea Park where the roof is gable and windows are original single-pane, immediate savings may be more modest. But the inspection identifies exactly which upgrades would move the needle and by roughly how much. A Winter Park homeowner who finds out their gable roof limits their credits can use that information to evaluate whether a future reroof conversion to hip geometry pencils out against the long-term insurance reduction. That’s not a bad thing to know.

Anyone who replaced their roof after Ian and hasn’t had a new inspection done: that updated report may produce meaningfully better credits than whatever was on file for the old roof. Don’t assume the savings are already being applied.

[Note to editors: Obtain 2–3 real homeowner before/after premium examples — Winter Park, Conway, and Lake Nona would give useful geographic spread — before publishing the savings figures above as anything more than benchmarks. Citizens’ current credit schedule for Orange County should also be confirmed with a local independent agent.]

How Much the Inspection Costs in Orlando

[Note to editors: Confirm current 2024–2025 quotes directly with AmeriSpec Orlando, Florida Home Inspections of Central Florida, and Waypoint Property Inspection before publication.]

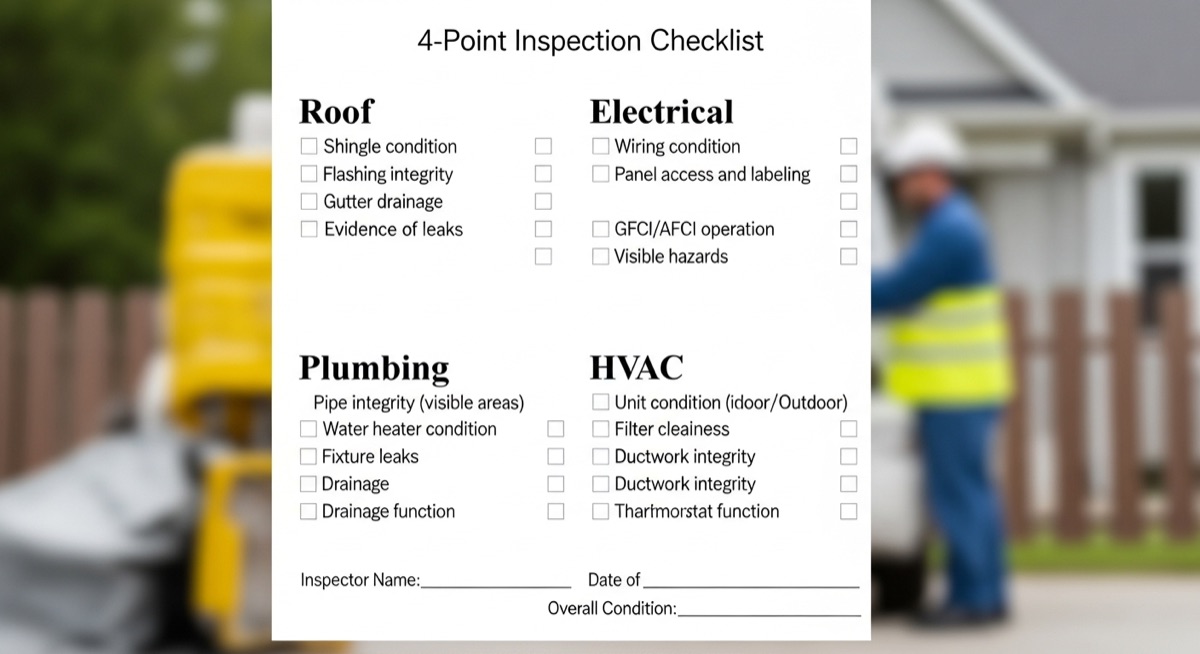

A standalone wind mitigation inspection typically runs $75 to $150 for a standard single-family home in Orange County. Homes with complex roof geometry, multiple structures, or difficult attic access may be quoted higher.

For most older Orlando homes, bundling this with a 4-point inspection makes practical sense. The 4-point covers the roof, electrical, plumbing, and HVAC systems — separately required by most Florida insurers when writing or renewing a policy on a home built before roughly 1998 to 2000. Since both inspections require the same licensed professional and the same attic access, combining them in one appointment saves a separate trip fee. The combined cost typically runs $125 to $200.

A homeowner in Pine Hills shopping for new coverage on a 1985 home and told by a carrier they need both inspections before the policy can be bound is a very common situation. Schedule both at once. And the fee is worth holding in context: if the completed OIR-B1-1802 reduces your annual premium by several hundred dollars, even the upper end of the standalone range is recovered within the first few months.

How Long the Report Is Valid — and When You Need a New One

There’s no statutory expiration on the OIR-B1-1802 under Florida law. Most insurers — including Citizens — treat wind mitigation reports as valid for five years from the inspection date, after which they require an updated inspection to continue applying credits.

More immediately relevant for many Orange County homeowners: a roof replacement voids your existing report for practical purposes, regardless of how recently it was completed. The inspection captures your roof’s features as they existed at the time. If you’ve replaced the roof since then — even recently — your old report no longer accurately describes your home. Your insurer is entitled to require a new inspection, and in most cases will.

This applies directly to the large number of Central Florida homeowners who replaced their roofs in 2022 and 2023 after Ian. If you had an existing wind mitigation report on file before the replacement, that report no longer represents your current home. The good news is that a new roof installed under current permitting often qualifies for better credits than the old one did. Getting an inspection on the new roof isn’t just bureaucratic renewal — it frequently produces a lower premium than the report it replaces, which is a decent outcome after an expensive reroof.

If you’re not sure whether your report is still being honored, your insurance agent can check whether the report on file is within their accepted validity window.

When to Schedule — and What to Do With the Report

Complete the inspection before your policy renewal. If possible, complete it before June 1. Florida’s hurricane season runs June 1 through November 30, and insurers process renewals on a rolling basis. Submitting a completed OIR-B1-1802 before your renewal date allows the credits to apply to the full upcoming policy year rather than being prorated. An inspection completed in March or April, submitted with renewal paperwork in May, means twelve full months of savings from day one.

The submission process is direct. When the inspection is complete, the inspector gives you the signed, completed OIR-B1-1802. You keep a copy and submit it to your insurance company — not to a government office, not through the inspector. Directly to your insurer. If you have an independent agent, they can submit it on your behalf and help you read how each line item affects your premium calculation, which is genuinely useful if you’ve never looked at one of these forms before. For Citizens policyholders, the report goes through your agent or directly to Citizens, and credits apply at the next renewal.

Wind mitigation credits stay on your policy as long as you have a valid report on file. When your report approaches the five-year mark, scheduling a renewal inspection is routine maintenance — the same logic as servicing your HVAC before it fails rather than after.

The Bottom Line

The inspection costs $75 to $150, or $125 to $200 bundled with a 4-point. It takes a few hours. What it produces is a state-standardized form documenting how well your home resists wind damage — and depending on your roof shape, how the deck is nailed, how the roof connects to the walls, and whether your windows and doors are impact-rated, that form can cut the wind portion of your annual premium by anywhere from a modest amount to well over $1,000 a year.

For older homes in Conway, Pine Hills, and Winter Park, it tells you exactly what you have and which upgrades are worth pursuing. For newer homes in Lake Nona and Horizon West, it documents credits those homes likely already qualify for but aren’t receiving because no one filed the form. For anyone who replaced their roof after Ian: get a new inspection. The updated documentation often comes back better than the old one.

In a market where homeowners insurance in Central Florida has become genuinely painful, this is about as clear a value proposition as you’re going to find — and unlike most things in insurance, it’s one you can actually act on.