What to Know About Flood Zones in Orlando

A neighborhood-by-neighborhood guide to Orlando's high-risk flood zones, how to look up any property on FEMA's maps, and what flood insurance actually costs in 2024 — including a discount most poli…

What to Know About Flood Zones in Orlando

A neighborhood-by-neighborhood guide to Orlando’s high-risk flood zones, how to look up any property on FEMA’s maps, and what flood insurance actually costs in 2024 — including a discount most policyholders don’t know to ask for.

When Hurricane Ian made landfall near Fort Myers on September 28, 2022, most attention focused on Lee County’s catastrophic storm surge. But Ian didn’t stop at the coast. As the storm tracked northeast across the Florida peninsula, it dumped record rainfall across Orange County, flooding streets and living rooms in neighborhoods that hadn’t been flagged in any real estate listing, any seller disclosure, or any conversation with a mortgage lender as particularly high-risk.

The financial consequence was blunt: standard homeowners insurance policies do not cover flood damage. They never have. Homeowners who had spent years paying for comprehensive coverage found themselves filing claims only to be told the water that destroyed their floors, walls, and contents was a flood loss — and flood losses require a separate policy they didn’t have. Some of those homeowners had been in their houses for decades.

Wind damage is typically covered. Flood damage is never covered by a standard homeowners policy in Florida. No exceptions. Understanding your property’s flood zone before you close isn’t just useful — it’s a financial decision with real consequences if you skip it.

What FEMA’s Zone Labels Actually Mean

FEMA designates flood zones through Flood Insurance Rate Maps, or FIRMs, maintained by the Map Service Center and updated on a rolling basis. Four zone designations appear with regularity in the Orlando area, each carrying specific legal and financial implications.

Zone AE is the one to pay closest attention to. It denotes a Special Flood Hazard Area with a 1% annual chance of flooding — the “100-year floodplain” — where a Base Flood Elevation (BFE) has been established in feet above sea level. Federal law requires flood insurance on any property in Zone AE that carries a federally backed mortgage: Fannie Mae, Freddie Mac, FHA, or VA. This requirement cannot be waived at closing and is not the lender’s discretionary call. If the mortgage is federally backed and the structure sits in an AE zone, flood insurance is mandatory. No negotiating it away.

Zone AH also qualifies as a Special Flood Hazard Area, but applies to areas subject to shallow ponding rather than riverine or sheet flooding. The mandatory purchase requirement applies here too.

Zone X covers areas outside the Special Flood Hazard Area. Moderate-risk X zones carry a 0.2% or lower annual flood chance; minimal-risk X zones carry even lower probability. Lenders don’t require flood insurance for Zone X properties — but here’s what gets glossed over in most real estate conversations: Ian proved that “not required” and “not needed” are not the same thing. A Zone X designation may keep you out of the mandatory insurance requirement. It does not mean your neighborhood cannot flood.

Zone VE — coastal velocity wave zones — applies to oceanfront Florida. Not relevant to central Orlando.

How to Look Up Any Orlando Property’s Flood Zone Before You Make an Offer

This search takes under five minutes. It should be as routine as pulling the county property appraiser record or scheduling an inspection. If you’re buying in Orlando and you haven’t done it, you’re missing a step.

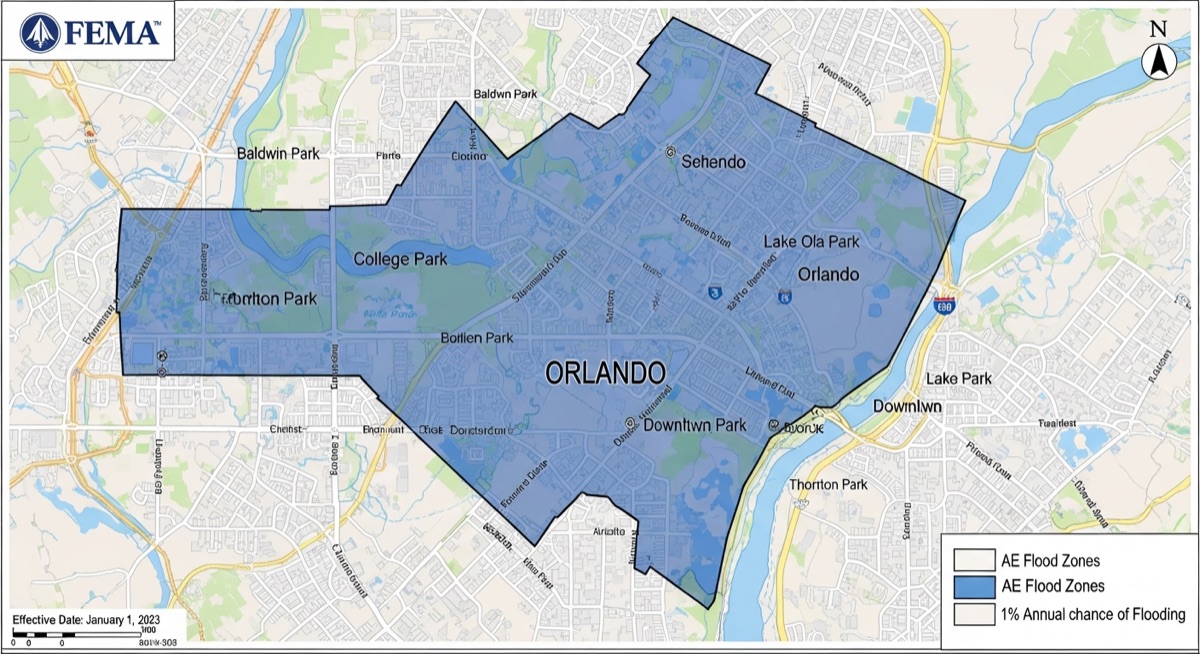

Go to msc.fema.gov, FEMA’s Map Service Center. Enter the property address. FEMA will return the current Flood Insurance Rate Map panel for that location. Orange County parcels fall under FIRM panel prefix 12095 — useful if you’re searching by panel rather than address.

When the map loads, find the zone designation (AE, AH, X, etc.) and, if the property is in a Special Flood Hazard Area, the Base Flood Elevation in feet. The BFE is the elevation at which floodwater is expected to reach in a 1% annual chance flood. How high your first floor sits above or below that number is the single most important variable in calculating your flood insurance premium. A property with a first floor one foot below BFE will pay substantially more than one sitting two feet above it — sometimes several hundred dollars a year. That gap adds up fast over a 30-year mortgage.

Cross-reference what you find with the Orange County Property Appraiser’s site (ocpafl.org), which displays parcel-level data and helps confirm the legal property boundaries you’re comparing against the FEMA panel.

One important caution: FIRM panels carry an effective date, and FEMA revises maps on a rolling cycle. Before relying on a map for a financial decision, confirm you’re viewing the current effective version. Check FEMA’s Flood Map Changes Viewer for any pending revisions — called Preliminary FIRMs or Letters of Final Determination — that could reclassify the property after you close. A property currently in Zone X can be moved into AE under a pending revision you wouldn’t otherwise know about. It happens, and it’s not a pleasant surprise to receive after closing.

The Orlando Neighborhoods in High-Risk Flood Zones

Most general-audience coverage of Florida flood risk defaults to vague references to “low-lying areas” or “lakefront property.” Here are named neighborhoods with specific risk context. All designations require address-level verification at msc.fema.gov — the map is the only definitive source.

Pine Hills (ZIP 32808) carries some of the highest flood exposure in Orange County’s unincorporated areas. The neighborhood is flat, drainage infrastructure is aging, and proximity to Lake Johio and Lake Fairview has produced AE-designated parcels throughout. Buyers here should treat FEMA map verification as mandatory before any offer — not something to circle back to.

Conway and Belle Isle, south of downtown, present some of the county’s most clearly defined flood exposure. The Lake Conway chain is a large, interconnected system, and AE-designated parcels run along Conway Road and Hoffner Avenue in documented patterns. The neighborhood has drawn real in-town development interest in recent years. Worth saying plainly: its popularity doesn’t change where the water goes in a heavy storm. Map the flood designations before negotiating price.

Winter Park lakefront lots on Lakes Virginia, Maitland, and Osceola require careful parcel-level analysis. Interior Winter Park — Baldwin Park, the upland neighborhoods — tends toward lower risk. Waterfront lots on the Winter Park Chain are a different calculation entirely. A $500,000 property carries a real estate waterfront premium that has nothing to do with its flood insurance premium, which could run $2,000 or more annually if first-floor elevation falls below BFE. Buyers sometimes discover the second number after they’ve already committed to the first.

Colonialtown and Mills 50, east of downtown, include AE-designated areas near Lakes Rowena and Druid. This is one of Orlando’s most competitive in-town markets. That competition has sometimes led buyers to skip flood zone verification — a decision that can mean $1,500 to $2,000 in annual insurance costs that were never factored into the property’s real carrying cost. Don’t let a tight offer deadline push you past a five-minute map check.

Azalea Park and Dover Shores, east of Conway, carry risk tied to Econlockhatchee tributary drainage and Lake Underhill. These are neighborhoods where flood zone status rarely comes up in the sales conversation. A property without a lake in sight can still sit in an AE zone because of sheet-flow drainage patterns and tributaries that aren’t obvious from the street — or from a listing photo.

East Orange County near the St. Johns River floodplain — including areas approaching the county’s eastern boundary — encompasses some of the broadest AE flood mapping in the metro area. The St. Johns River’s low-gradient floodplain is wide and flat, and properties here can carry significantly higher flood insurance costs even when the property itself isn’t directly riverfront.

For comparison, interior Lake Nona, Waterford Lakes, Hunters Creek, and Baldwin Park (the former Naval Training Center site) generally carry Zone X designations, reflecting modern engineered drainage and managed grade. Ian demonstrated that Zone X doesn’t mean flood-proof — but these areas typically fall outside mandatory purchase requirements and often qualify for lower-cost preferred-risk policies.

| Neighborhood | Primary Zone Designation | Key Risk Factor |

|---|---|---|

| Pine Hills (32808) | AE (portions) | Flat topography; Lakes Johio, Fairview |

| Conway / Belle Isle | AE | Lake Conway chain; Conway Rd, Hoffner Ave |

| Winter Park lakefront | AE (waterfront) | Winter Park Chain of Lakes |

| Colonialtown / Mills 50 | AE (portions) | Lakes Rowena and Druid |

| Azalea Park / Dover Shores | AE (portions) | Econ tributaries; Lake Underhill |

| East Orange County | AE (broad) | St. Johns River floodplain |

| Lake Nona interior | X (generally) | Engineered drainage |

| Waterford Lakes | X (generally) | Master-planned drainage |

| Hunters Creek | X (generally) | Engineered stormwater |

| Baldwin Park | X (generally) | Former NTC; engineered stormwater |

All designations require address-level verification at msc.fema.gov.

What Flood Insurance Actually Costs in Orlando

No homeowners insurance policy — not Allstate, not State Farm, not anyone writing standard coverage in Florida — covers flood damage. Flood insurance is purchased separately, either through FEMA’s National Flood Insurance Program (NFIP) or the private market. This isn’t a fine-print technicality. It’s a separate purchase with its own premium, its own application, and its own coverage limits.

The post-Risk Rating 2.0 national NFIP average sits around $888 per year. Florida’s higher-risk environment pushes that number up, with most policyholders seeing premiums somewhere in the $958 to $1,200 range — though that’s a rough mean that hides wide variation by property. For Orlando Zone AE single-family homes with roughly $250,000 in structure value, agents writing in this market quote $1,200 to $2,500-plus annually. The spread comes almost entirely from how the structure’s first-floor elevation compares to BFE. Two houses on the same block can carry meaningfully different premiums depending on how they were built relative to grade.

Zone X preferred-risk policies have historically run $400 to $700 per year, though Risk Rating 2.0 has complicated that range somewhat.

The private market matters more than many buyers realize. Tampa-based carriers including Kin Insurance and Neptune Flood have, for well-elevated properties, undercut NFIP pricing by a real margin. For a home sitting two or more feet above BFE in a Zone AE area, a private policy may cost less than NFIP while providing equivalent or better coverage terms. Get competing quotes. An independent agent who writes both NFIP and private market policies isn’t optional here — it’s the standard of care for any Orlando buyer in a flood-affected zone.

One NFIP detail that trips up buyers consistently: the program caps building coverage at $250,000 and contents coverage at $100,000, and the two are purchased separately. A buyer who closes on a Zone AE property, buys NFIP building coverage, and assumes contents are included has made an expensive mistake. The contents policy is a separate election with a separate premium. A house full of furniture, electronics, appliances, and personal property can easily exceed $100,000 in value — and that’s before counting anything in the garage.

Risk Rating 2.0 Changed What You Pay — and Not Always the Way You’d Expect

FEMA’s Risk Rating 2.0 took effect in October 2021 for new policies and October 2022 for renewals. It replaced a decades-old NFIP pricing formula that leaned primarily on flood zone and elevation with a system that incorporates distance to water, flood frequency, cost to rebuild, and multiple flood type risks. The results genuinely surprised people — in both directions.

Some Orange County homeowners in Zone AE saw premiums drop under the new methodology. Their properties were elevated enough and far enough from water that the more detailed calculation worked in their favor. Some Zone X homeowners saw increases, because Risk Rating 2.0 identified risks the old binary zone system had missed entirely. A property that paid $500 annually under the old formula might now pay $750 with no zone change at all. If you haven’t looked at your flood policy since before 2022, have that conversation with your agent.

One safeguard for existing policyholders: FEMA caps annual NFIP premium increases at 18% for existing policies. This matters because the trajectory — where the cost is headed over five to ten years — may be as important as the first-year number. A policy already priced below its “full risk rate” under Risk Rating 2.0 will increase at 18% annually until it gets there. A buyer inheriting a low current premium should ask directly whether it reflects full risk or is still climbing toward it. Agents don’t always volunteer that information unprompted.

The CRS Discount — Money Policyholders May Not Be Collecting

This is the one that genuinely surprises people. FEMA’s Community Rating System rewards jurisdictions that exceed minimum floodplain management requirements with discounts on NFIP premiums for policyholders in those jurisdictions. The discount runs from 5% to 45% depending on the community’s CRS class rating.

Both Orange County and the City of Orlando participate. Orange County holds a CRS Class 6 or 7 rating, translating to a 15% to 20% NFIP premium discount. The City of Orlando holds a Class 5, which means a 25% discount on NFIP premiums. On a $1,500 policy, that’s $375 per year. It’s real money — and it’s money policyholders who don’t know to check for it may not be receiving.

Verify both figures directly before relying on them. Orange County Floodplain Management can be reached through Orange County Public Works at 407-836-7995. The City of Orlando’s stormwater division is at 407-246-2170.

Here’s the practical catch: which jurisdiction does your property actually sit in? A parcel with an Orlando mailing address may be in unincorporated Orange County. A parcel with a Winter Park or Ocoee mailing address falls under a different municipality’s CRS classification entirely. Your jurisdiction determines your discount. Verify this with your agent before closing — mailing address and municipal jurisdiction are not the same thing, and the difference can change your premium.

How to Fight a Flood Zone Designation — and When It’s Worth It

If you believe your property has been incorrectly mapped into a Special Flood Hazard Area, you can formally challenge that designation through a Letter of Map Amendment, or LOMA. The challenge is based on the position that your structure’s lowest adjacent grade sits above the Base Flood Elevation.

A LOMA, if FEMA approves it, removes the property from the mandatory flood insurance purchase requirement. Filing costs nothing. What it requires is an Elevation Certificate from a licensed Florida land surveyor — a document certifying the elevation of your structure relative to the BFE. In the Orlando area, those certificates typically run $300 to $600. Even without a LOMA, a certificate showing a first floor well above BFE can directly reduce NFIP premiums, since elevation is a primary pricing variable under Risk Rating 2.0. That $400 document can pay for itself quickly.

Homeowners navigating this process should start with Orange County Floodplain Management at 407-836-7995. The office can explain where the property sits relative to the effective FIRM panel and whether a LOMA is likely to succeed given that specific parcel’s history. A property with a first floor demonstrably two feet above BFE has a reasonable shot. A property in a documented low-lying area with flood history does not — and it’s better to know that before spending money on paperwork.

LOMAs aren’t a blanket solution. A property that genuinely sits in a low-lying area isn’t getting pulled from the SFHA because someone filed paperwork. But for properties that ended up in an AE designation because of imprecise historical mapping, a LOMA is a legitimate and financially meaningful remedy.

Orlando’s Flood Season — When Risk Is Highest and Why the Calendar Matters

Orlando gets roughly 53 inches of rainfall annually, most of it between June and September. Summer convective storms regularly drop three to five inches in under an hour. On flat terrain with a