What Orlando Homeowners Are Actually Paying for Property Insurance in 2026

And which companies are still writing policies here — a ZIP-code-level look at Orange County premiums, Citizens eligibility, carrier availability, and whether a wind mitigation inspection is worth …

What Orlando Homeowners Are Actually Paying for Property Insurance in 2026

And which companies are still writing policies here — a ZIP-code-level look at Orange County premiums, Citizens eligibility, carrier availability, and whether a wind mitigation inspection is worth the money

Hurricane season opened June 1. If you haven’t reviewed your homeowners insurance since last year’s renewal notice arrived, you’re already behind. The Orlando market looks meaningfully different in 2026 than it did eighteen months ago. Carriers that were actively writing business in Orange County have quietly pulled back. Citizens Property Insurance has tightened its eligibility rules in ways that catch homeowners off guard. And the premium trajectory that started climbing in 2021 hasn’t reversed — despite the reform legislation Tallahassee passed in the 2022 special session and 2023 regular session, despite what some lawmakers promised, despite everything.

This piece is for Orange County homeowners who want real numbers and real carrier names, not a quote form and a statewide average pulled from a national aggregator. The specifics below come from conversations with local independent agents placing business in Central Florida right now, OIR rate filing records available at floir.com, and publicly available Citizens policy data. Where figures involve individual agent or inspector estimates, that context is noted.

What a $350,000 Orange County Home Is Actually Costing to Insure Right Now

The figure most national sites cite for Florida homeowners insurance reflects a statewide blend that heavily weights South Florida’s coastal exposure. It doesn’t capture what’s happening in Orange County. For a mid-range home insured for $350,000 in replacement cost — not market value, a distinction that matters and that I’ll get to — expect to pay somewhere between $3,200 and $5,500 per year in 2026, depending on factors that vary a lot by property.

Construction era matters enormously. A newer Lake Nona build — say a 2018 single-family home in 32827 with a hip roof, concrete block construction, and current opening protections — can land closer to $2,400 to $3,200 with a competitive private carrier. A 1990s home in Ocoee with a gable roof and an original or once-replaced roof now approaching age threshold tells a very different story. It can push past $4,500 — sometimes $6,500 or higher — before any surcharges for roof condition. That’s close to a $4,000 spread on homes with similar market values. Worth knowing before you assume your neighbor’s premium resembles yours.

Roof age alone — not roof damage, just age — is the single biggest premium lever most homeowners don’t fully understand until they’re staring at a non-renewal notice. A home with a 2012 roof is now 13 or 14 years old and approaching the zone where carriers start pricing defensively. A home with a 2004 roof is already past it. Most carriers won’t write homes with roofs 25 years or older, and the surcharges start well before that threshold.

The replacement cost figure on your declarations page also matters more than most homeowners realize. If your insurer has updated that estimate to reflect current construction costs — and most have, because labor and materials spiked substantially after 2020 — your premium base is higher than it was even if your coverage limits look the same. Check your current declarations page against last year’s. For many Orange County homeowners, the insured replacement value increased. Sometimes by a lot.

Why Your Renewal Went Up Even Though You Never Filed a Claim

This is the question local agents field constantly. It’s a fair one. Individual claims history matters, but it’s often not the dominant driver in the current Florida market. Understanding what’s actually moving your premium is the difference between a renewal notice that makes sense and one that feels arbitrary.

Reinsurance costs are the part most people don’t see. Insurance companies buy their own insurance — reinsurance — to cover catastrophic loss years. After back-to-back active hurricane seasons, multiple Florida carrier insolvencies, and global reinsurance market tightening, the cost of that coverage has gone up substantially. Carriers pass those costs to policyholders through OIR-approved rate increases. Those increases apply to every policyholder in a given rating territory, regardless of whether you personally filed a claim last year. You’re not being singled out. You’re just in the pool.

Carrier exits are concentrating risk across fewer companies. More than 15 property insurers have exited Florida or gone insolvent since 2020. Each time a carrier exits, its book of business has to go somewhere — typically to Citizens or to the remaining private carriers, which then carry more concentrated risk and face less competitive pressure to keep rates reasonable. The carriers still writing business in Central Florida know they have pricing power that didn’t exist four years ago. They’re using it.

You can cross-reference any renewal increase against OIR records at floir.com using their rate filing search tool. Looking it up tells you whether the increase was filed and approved, or whether something else is driving it. Most of the increases Orange County homeowners have seen are legitimately OIR-approved — which doesn’t make them more affordable, but does mean they’re not arbitrary, and the records are public.

The 2022–2023 reform legislation didn’t deliver the immediate premium relief some lawmakers promised. The Assignment of Benefits reform and the litigation changes passed in those sessions were real — I’m not dismissing them. Most insurance attorneys and industry analysts believe they’ll reduce claims costs over time. But reinsurance contracts renew annually, carrier portfolios take time to stabilize, and the legal system takes longer than one cycle to recalibrate. The realistic estimate from people who track this closely is three to five years before the reforms fully appear in retail premiums. Anyone who was promised immediate relief was misled, and plenty of people were.

Which Insurance Companies Are Still Writing New Policies in Central Florida

This is the question national aggregators won’t answer, because their business model is selling your contact information rather than giving you useful information. Here’s what local independent agents report about carrier availability in Orange County as of mid-2026.

| Carrier | Status in Orange County | Notes |

|---|---|---|

| Universal Property & Casualty | Actively writing | One of the largest private writers left in Florida; rates vary significantly by property |

| HCI Group (Homeowners Choice) | Actively writing | Florida-based; agents report solid availability for qualifying properties |

| Slide Insurance | Actively writing | Has been absorbing Citizens depopulation assignments; review terms before accepting |

| Kin Insurance | Actively writing | Direct-to-consumer model; competitive for newer construction with documented wind mitigation |

| Citizens Property Insurance | Writing (eligibility required) | See Section 4; available doesn’t mean cheapest |

| Heritage Insurance Holdings | Restricted | Has significantly reduced new-policy writing in Central Florida; confirm before applying |

| Bankers Insurance Group | Exited or severely restricted | Agents report inability to place new business |

Carrier availability shifts quickly — sometimes within a single quarter. Before you spend time on an application, ask your agent directly: “Are you currently placing Orange County homeowners business with this carrier?” A hedged answer means restricted. This list reflects what agents active in the market are reporting as of mid-2026; it’s not a guarantee for your specific property.

The private market is thinner than it looks. Universal Property and Homeowners Choice are carrying a disproportionate share of what’s left in Central Florida. Slide has been growing its Florida book partly through Citizens takeout assignments — worth reading the offer terms carefully if one arrives. Kin’s technology-forward model can produce competitive quotes for lower-risk profiles, particularly newer construction with wind mitigation features already documented. If your home qualifies, it’s worth getting their number.

Citizens Insurance — Who Qualifies, What It Costs, and What the Depopulation Push Means for You

Citizens is Florida’s insurer of last resort, created by statute to provide coverage when the private market won’t. Most competing content either ignores the eligibility rules or gets them wrong.

To qualify for Citizens, a homeowner generally must be unable to find a comparable private market policy for less than 20% more than the Citizens rate. Citizens isn’t automatically available just because private market options are expensive — you have to be in a situation where private quotes exceed Citizens by that specific threshold. Your agent must document this through the Citizens Clearinghouse, a mandatory process where agents are required to check for private market availability before binding Citizens coverage. If an agent tells you you’re Citizens-eligible without running the Clearinghouse, that’s a problem.

Citizens also has a replacement cost cap for Personal Lines coverage at approximately $700,000 for 2025–2026 — confirm the current threshold directly with Citizens or your agent. This matters in Windermere, Dr. Phillips, and parts of the Winter Park corridor where replacement costs on larger or higher-finish homes can exceed that number. If your home’s insured replacement value crosses that line, Citizens isn’t an option regardless of the rate differential.

Here’s where the depopulation rules catch people off guard. Citizens is actively working to reduce its policy count by facilitating takeout offers from private carriers. If a private carrier submits an offer to take your Citizens policy, declining that offer does not automatically preserve your Citizens eligibility. Depending on the offer terms, Citizens may still remove you from its rolls. If you receive a takeout letter, read it carefully and talk to your agent before declining. The consequences of saying no can be different from what you’d expect, and this catches people by surprise every year.

Whether Citizens is actually cheaper than private carriers is genuinely counterintuitive, and I’d encourage you not to assume either way. For Orange County homes with strong wind mitigation features — hip roofs, solid deck attachment, secondary water resistance underlayment — the credits a private carrier applies can bring a private quote below a Citizens rate. Get both quotes simultaneously before assuming Citizens is the better deal. For a broader look at how these rate pressures connect to coverage decisions across the county, our Florida property insurance rate increases and what they mean for homeowners unpacks the legislative and market context in more detail.

Does a Wind Mitigation Inspection Actually Save Money — the Orange County Math

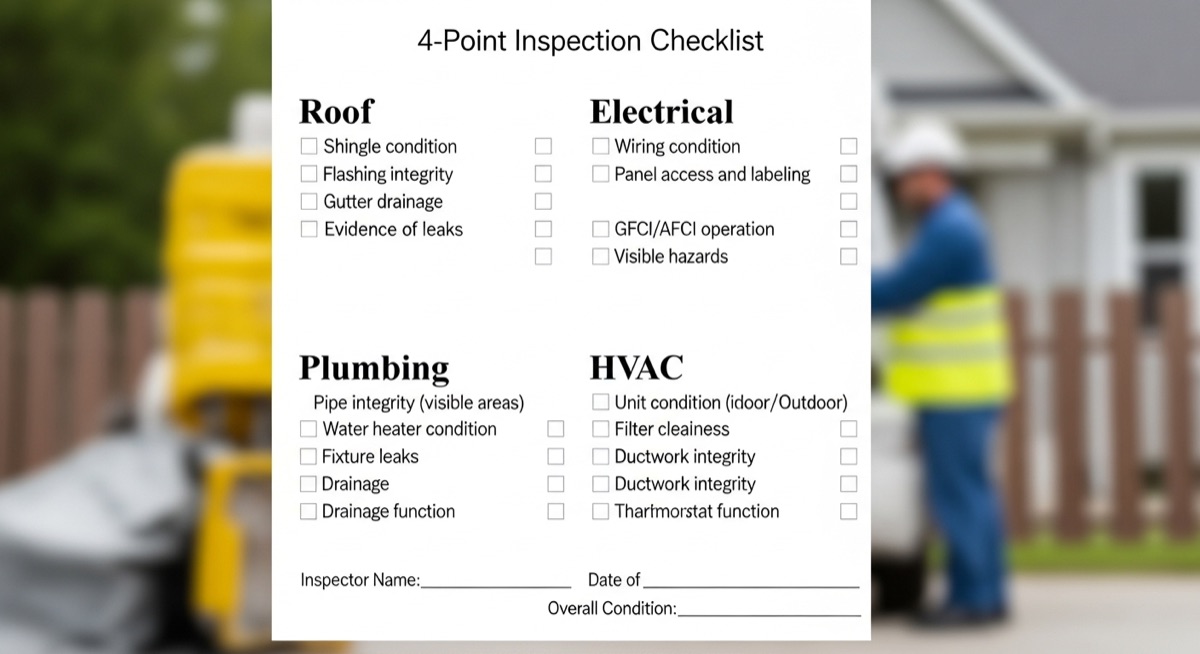

A wind mitigation inspection is a formal assessment of a home’s wind-resistant features, performed by a licensed inspector and submitted to your insurer on a standardized Florida form. Under Florida statute 627.0629, insurers are required to apply wind mitigation credits — it’s not discretionary. The question is whether the inspection fee is worth the savings.

In Orange County, a standalone wind mitigation inspection runs $150 to $250 from licensed inspectors. Bundled with a 4-point inspection (which many carriers now require separately for older homes), the combined cost is typically $275 to $350. The inspection pays for itself quickly if the credits are meaningful — and often they are. What Orlando homeowners need to know about 4-point inspections — including what each section covers and how results affect carrier decisions — is covered in our home & property coverage for Orange County residents.

The three features that generate the largest credits here: a fully hip roof (all sides slope to a ridge or point, no vertical gable ends), 8d nail deck attachment at 6-inch spacing in the field, and secondary water resistance underlayment — a self-adhering modified bitumen membrane applied to the roof deck before shingles. Orange County is in the Florida Building Code’s inland wind zone, not the coastal high-velocity hurricane zone, but wind mitigation credits still apply.

Here’s what the return looks like in practice. A $200 inspection that documents a hip roof, qualifying deck attachment, and SWR could produce annual premium savings anywhere from $200 to $800, depending on your carrier and base premium. At $400 in annual savings, the inspection pays for itself in six months. At $800 — realistic for a higher-premium policy that previously had no wind mitigation credits on file — the payback is essentially immediate. Agents describe clients who had no idea how much they were leaving uncaptured.

Wind mitigation reports are valid for five years. If you’ve replaced your roof in the last year or two and haven’t ordered a new inspection, you’re almost certainly missing credits. A new roof often qualifies for deck attachment and SWR documentation that an old inspection couldn’t capture because the old roof predated those features. Order the new inspection before your next renewal, not after. Submitting a new report mid-policy term triggers an immediate premium adjustment at most carriers — you don’t have to wait for renewal to see the savings.

How Your Neighborhood Changes Your Rate — and Your Options

Underwriters price by territory and sometimes by ZIP code, based on claims history, construction vintage, and proximity to hazards. In Orange County, those differences are real and measurable.

32827 (Lake Nona) has newer construction, favorable wind ratings, and lower claims history in a relatively young development area. A comparable home here tends to sit at the lower end of the premium range. The housing stock is younger, hip roofs are more common, wind mitigation features are frequently already documented, and carriers are actively competing for this business — which is part of why Lake Nona homeowners are sometimes getting quotes that feel almost reasonable by 2026 standards.

32808 (Pine Hills) presents a different underwriting profile: older housing stock, mid-century construction in some pockets, higher area claims history, and a roof age problem that’s structural rather than individual. A large share of the housing stock has roofs approaching or past the 20-year mark at the same time, creating a concentration risk that carriers treat as a ZIP-level issue. That affects your individual premium even if your specific roof is in fine shape. Premiums for a comparable home run meaningfully higher here than in Lake Nona, and carrier appetite for new policies is more selective.

32812 (Conway / Belle Isle corridor) sits in the middle. Mid-century construction, significant roof age clustering, and a wide mix of construction types mean the premium spread runs wide within the same ZIP. A recently re-roofed home with documented wind mitigation might quote comparably to a Lake Nona home. A home with a 2002 roof and gable geometry might be struggling to find coverage at any reasonable price. Same ZIP code, completely different situation depending on the specific property.

Dr. Phillips and Windermere introduce a separate issue beyond wind: lake-adjacent properties in both corridors are increasingly drawing scrutiny for flood exposure that doesn’t trigger mandatory NFIP purchase requirements but creates real financial risk. Private flood riders are being recommended for properties near the Butler Chain and the Windermere lake system even when a lender isn’t requiring flood insurance. This adds a cost layer that doesn’t appear in standard homeowners premium comparisons, but it belongs in your total insurance budget. Ask about it specifically if you’re in those neighborhoods.

The Roof Age Tripwire — and What to Do If Your Home Is in the Danger Zone

This is the most urgent issue facing a large segment of Orange County’s homeownership base right now. If your home was built in the 1990s or early 2000s and the roof hasn’t been replaced, you may be approaching — or past — the threshold where carriers will act. The non-renewal letters are real.

Most carriers won’t write homes with roofs 25 years or older. The surcharges for aging roofs are not trivial — 30% to 50% added to your base premium appears regularly for homes approaching that threshold. What people miss is that the surcharge schedule often starts at year 18 or 19, not year 20. By the time you hit the headline number, you’ve already been paying extra for a couple of years.

A 4-point inspection covers four systems: roof, electrical, HVAC, and plumbing. Agents routinely require it for any home 30 years or older before shopping the property to private carriers. A roof section that shows significant wear, curling shingles, or fewer than three years of remaining life will frequently trigger a decline or non-renewal regardless of everything else about the home.

If a carrier non-renews you due to roof age, your options narrow fast: replace the roof, try Citizens (subject to eligibility), or look for a surplus lines carrier willing to write the property at a substantially higher premium. None of those options is good. Replacing the roof before a non-renewal arrives gives you timing control, lets you shop the property to multiple carriers, and lets you get the wind mitigation inspection ordered immediately after completion to capture maximum credits. If you’re evaluating replacement costs before committing, the roof replacement cost breakdown for Orlando homeowners covers current labor and materials pricing in detail.

If your roof is approaching 20 years old and you haven’t had a specific conversation with your agent about its insurability, that conversation needs to happen before your next renewal cycle. Not after.

Independent Agent vs. Direct vs. Aggregator — How to Actually Shop This Market

The structure of how you shop matters more in this market than it did five years ago.

National lead-gen aggregators promise five quotes in three minutes. What they’re actually doing is selling your contact information to agents and carriers willing to pay for it. The quotes they surface are frequently not the most competitive options for your specific property. They can’t navigate the Citizens Clearinghouse process, tell you which carriers are currently accepting applications in your ZIP code, or explain how much appetite a given carrier has for new business this quarter. The three-minute promise is a red flag, not a selling point.

Captive agents can only offer you their company’s product. In a market this distorted, that’s a genuine disadvantage.

Local independent agents who actively place homeowners business in Orange County can access multiple carriers, navigate the Citizens Clearinghouse requirement, and give you current information about which carriers are accepting applications for properties like yours. Ask any agent you contact: “Which carriers are you currently placing new homeowners business with in Orange County?” If they hesitate, or name carriers you can’t verify are active, that’s information. It usually means they haven’t placed business with that carrier recently — which tells you something about how current their market knowledge actually is.

The Citizens Clearinghouse process is one concrete reason local agents matter right now. Before an agent can bind Citizens coverage, they’re required to run your property through the clearinghouse system to document that private market options aren’t available within the 20% threshold. An agent who runs this regularly can tell you within a day whether Citizens is a realistic option or whether you should focus on private market alternatives. An agent unfamiliar with the process will slow you down at a moment when speed matters.

With hurricane season open, if you’re uninsured, underinsured, or facing a pending non-renewal, treat getting multiple quotes as genuinely urgent. The carrier picture can shift between when you start shopping and when you complete an application. That’s happened to people in this market.

What to Do Before You Call an Agent

The homeowners who get the most out of an agent conversation show up with their documents and questions organized. You don’t need to be an expert. You just need to not show up empty-handed.

Pull your current declarations page. Note the insured replacement cost — not the market value, which is a different number and a common source of confusion. Note your current carrier, your annual premium, and your policy expiration date. If you’re within 60 days of expiration and haven’t started shopping, start now.

Document your roof age. If you’ve had a replacement, find the permit or contractor invoice showing the installation date. If your roof is more than 15 years old and you don’t have documentation, consider ordering a 4-point inspection before calling agents — it tells you and potential carriers what condition the roof is actually in. If your roof was replaced recently, get a wind mitigation inspection ordered before your next renewal.

Look at your roof shape. Walk outside. A hip roof slopes down on all sides with no vertical triangular end walls. A gable roof has those triangular ends. This distinction affects your wind mitigation credits and how carriers underwrite the property.

Know your opening protections. Impact-resistant windows, hurricane shutters, panel protection for doors and garage — each can affect your wind mitigation score.

If you’re in Dr. Phillips, Windermere, or any lake-adjacent neighborhood, ask your agent specifically about private flood coverage options — not just whether your lender requires it, but whether the risk profile warrants it regardless.

Bookmark floir.com. The OIR rate filing search tool lets you verify whether a rate increase your carrier cited was actually filed and approved by the state. It’s public, it’s searchable by carrier name, and most people don’t know it exists.

The Orlando homeowners insurance market in 2026 is more expensive and more complicated than most residents expected when they bought. There’s no clean way to say that. But the rules aren’t arbitrary — they’re specific, they’re documented, and once you understand them, they’re workable. That’s the honest version.