Orlando Home Insurance Rates and Carriers in 2026

Which carriers are active in Orange, Seminole, and Osceola counties, what a Citizens depopulation letter really means, and what neighbors in 32825, 32836, and 32801 are paying this year

Orlando Home Insurance Rates and Carriers in 2026

Which carriers are active in Orange, Seminole, and Osceola counties, what a Citizens depopulation letter really means, and what neighbors in 32825, 32836, and 32801 are paying this year

If you opened a non-renewal notice or a Citizens assumption letter in the last few months, you already know the Florida home insurance market hasn’t returned to normal. Whatever normal was. Statewide legislative fixes have slowed the bleeding, but in Orange, Seminole, and Osceola counties, homeowners are still confronting premium shock, shrinking carrier choices, and paperwork they don’t fully understand.

This piece maps where the market actually stands in Central Florida in 2026: which companies are writing new policies here, what ZIP codes are paying, and what your options look like if you’re shopping from scratch. Some of it is frustrating to report.

Why Orlando’s Market Still Feels Broken

The hurricane that reset how reinsurers think about Central Florida wasn’t one that hit Orlando. It was Ian, which made landfall near Fort Myers in September 2022 and caused significant inland wind and tree damage in Orange County. If you were here for it, you remember the downed trees and the power outages that dragged on for days. Reinsurers remember it differently: they remember the claims.

Reinsurers — the companies that insure insurers — responded by pricing Central Florida as far more exposed than they had before. That repricing cascaded into admitted carrier withdrawals, rate increases, and a surge of homeowners into Citizens Property Insurance.

The carriers that exited or sharply reduced their Orlando-area footprint read like a who’s who of names that were common here a decade ago: Bankers Insurance, St. Johns Insurance, Avatar Property & Casualty, and FedNat all either became insolvent or pulled back from Florida between 2022 and 2024. Each exit pushed more policyholders toward Citizens, which was never designed to be a primary market.

The Florida Legislature passed SB 2-A in December 2022 and HB 837 in 2023, restricting assignment of benefits arrangements and one-way attorney’s fee arrangements that had fueled an explosion of roofing litigation and fraudulent claims. The reforms reduced litigation costs. Several carriers that had stopped writing new business in Florida have resumed, cautiously, in certain markets. Reinsurance costs have begun to moderate. But the savings haven’t reached most Orange County homeowners yet.

Rates filed and approved by the Florida Office of Insurance Regulation reflect carriers rebuilding reserves and capital cushions, not passing savings through to policyholders. The stabilization is real. The relief is not.

Which Carriers Are Actually Writing New Policies in Orange, Seminole, and Osceola

This is the question competing information sources consistently dodge by listing every company licensed in Florida rather than naming who will actually quote a home in your ZIP code right now. It’s one of the more maddening things about searching for this information online.

[Editor’s note: The carrier descriptions below are based on interviews with independent agents operating in the three-county area. Carrier appetites change; verify current availability with a licensed local agent and cross-check the Florida OIR’s admitted carrier list before binding.]

Universal Property & Casualty is actively writing new business in all three counties. Agents describe it as one of the more accessible markets for homes with roofs in the 12-to-15-year range, though it has tightened its roof age cutoffs in some East Orlando ZIP codes and will require documentation — typically a 4-point inspection — for roofs approaching 15 years.

Homeowners Choice (HCI Group) is writing new policies across all three counties and has been participating in Citizens depopulation rounds. It carries a Demotech financial stability rating. Homeowners with federally backed mortgages should verify the current rating at binding, since Fannie Mae and Freddie Mac require at least a Demotech A from Florida-domestic carriers. HCI writes concrete block construction and is more favorable on older roofs than some competitors — which matters more than it might sound in a county full of 1990s-era housing stock.

Security First Financial is active in Central Florida and gets mentioned by agents when a home doesn’t fit the mainstream admitted market: older construction, gable roofs, homes in ZIP codes with higher loss histories. Its rates are not low, but it writes business where others won’t. Sometimes that’s exactly what you need.

Slide Insurance expanded after the legislative reforms and is writing new policies in the three-county area. It has been among carriers active in Citizens takeout rounds and shows willingness to write homes that were recently nonrenewed by other carriers, though terms vary considerably by property.

Tower Hill Insurance writes in Central Florida but agents describe it as selective in 2026, particularly in areas with documented sinkhole activity and in ZIP codes where older homes with gable roofs dominate.

Citizens Property Insurance itself remains available but is no longer the automatic backstop it once was. The 20-percent eligibility threshold — Citizens cannot be your insurer if a comparable private market policy is available within 20 percent of Citizens’ rate — has constrained eligibility. If a private carrier will quote your home, you likely can’t choose Citizens. That used to sound like a good problem to have. For homeowners whose only private-market quote comes in at $6,000, it doesn’t feel that way.

State Farm significantly curtailed new homeowner policy writing in Florida following the post-Ian market disruption and is not a realistic option for most Orlando homeowners shopping in 2026. Allstate has similarly restricted new business in most of the state. Existing policyholders with either carrier may be renewed, but new applicants should not count on either company. I know that’s not what people want to hear — those are the names people trust — but it’s where things stand.

For mortgaged homeowners, Demotech ratings are a practical filter. Verify a carrier’s current rating before binding. Ratings can change; checking FLOIR’s admitted carrier list and Demotech’s published ratings at the time you bind is not optional.

What Your ZIP Code Does to Your Premium

The statewide average for Florida home insurance was roughly $3,600 to $4,200 annually as of 2024, but that number conceals enormous variation by location, home age, and construction type. It’s also useless to you if your specific house is the problem. The figures below are based on interviews with independent agents for a representative home: 2,000 square feet, concrete block construction, built in 2005, $350,000 replacement cost value. They reflect what agents report quoting in current market conditions. Treat them as directional, not as guaranteed quotes.

[Editor’s note: ZIP-code-level premium quotes require verification with local agents and FLOIR rate filings. Readers should obtain multiple quotes from licensed independent agents for their specific property.]

32825 — East Orlando / Waterford Lakes area: This ZIP is aging-roof territory. A 2005 build means a roughly 20-year-old roof, which is exactly the threshold where surcharges activate and some carriers decline to quote without a recent replacement. The difference a roof replacement makes here is not marginal. Agents report it can exceed $1,000 per year in premium savings. Homeowners shopping now need to plan on either replacing the roof before binding or accepting narrow carrier options and elevated premiums. Those are genuinely your only two choices.

32836 — Dr. Phillips / Sand Lake corridor: Higher-value homes in this ZIP drive higher premiums, but Dr. Phillips also has newer construction and a relatively favorable loss history. Hip-roof construction common in the area’s newer developments qualifies for wind mitigation credits, and agents note that some carriers are more competitive here because the roof age problem is less acute.

32801 — Downtown Orlando: This is primarily a condo market, which means the relevant product is an HO-6 policy, not a standard HO-3. HO-6 premiums are structurally lower than single-family premiums because the building exterior and common areas are covered under the HOA’s master policy. The gap between what the master policy covers and what the unit owner is actually exposed to is the real story in this ZIP — addressed below. Unit owners here frequently discover after a loss that they underinsured their personal improvements. That’s the worst possible time to find out.

32812 — Conway / Pine Castle: This area combines aging housing stock — much of it predating 1990 — with documented flood exposure in low-lying sections near Lake Conway. Parts of downtown (32801) and Ventura/Conway (32822) carry FEMA AE or X-500 flood zone designations; homeowners in adjacent 32812 should verify their specific flood zone status on FEMA’s flood map service. Agents describe 32812 as one of the harder-to-place ZIP codes in the county for standard admitted carriers. Surplus lines may be the only realistic option for pre-1990 construction. Properties in flood zones need separate flood insurance regardless of insurer, and the cost-benefit analysis shifts considerably when your home sits in an X-500 zone.

Citizens Depopulation — What That Letter in Your Mailbox Actually Means

Citizens Property Insurance has been shrinking its policy count deliberately through a process called depopulation: private carriers agree to “assume” blocks of Citizens policies, removing those homeowners from the state-backed insurer.

If you received a letter saying a company you’ve never heard of is assuming your Citizens policy, here is what’s actually happening — and why the clock matters more than people realize.

Florida law gives Citizens policyholders typically 30 days to reject the assumption and stay with Citizens, but only if the assuming carrier’s premium is more than 20 percent higher than your current Citizens rate. If the private carrier’s rate is within 20 percent, you cannot opt out and remain Citizens-eligible. Read the letter carefully for the opt-out deadline. Agents report that homeowners frequently miss it. Thirty days goes fast when the letter sits in a pile of mail.

Before you accept the new policy, verify that your optional coverages carry over. If you had sinkhole coverage, flood endorsements, or scheduled personal property on your Citizens policy, confirm explicitly with the assuming carrier that those coverages appear in the new policy. Do not assume they transfer automatically. Some carriers strip optional coverages in the assumption process, and if you don’t catch it in the 30-day window, you’re stuck.

Homeowners Choice and Slide Insurance have been identified as participants in Citizens depopulation rounds affecting Orange, Seminole, and Osceola counties, though the specific carriers active in any given round change. Citizens publishes its depopulation round schedules on its website; verify current round participants directly with Citizens or your agent.

The 20-percent rule has changed the calculus significantly. Before recent reforms, Citizens functioned as a last resort that most homeowners could fall back on. Now that access is narrowed considerably. Independent agents report that homeowners who were dropped by a private carrier and expected to fall back on Citizens are sometimes finding they don’t qualify because at least one carrier in the admitted market will quote them — even at a price they consider unaffordable. I don’t think there’s a clean answer for people stuck in that position.

Roof Age Is the Underwriting Tripwire in East Orlando

No single variable is doing more to disrupt coverage for Orlando homeowners right now than roof age. Homes built between 1990 and 2010 — a large portion of the East Orlando (32825, 32828), Ocoee (34761), and Kissimmee housing stock — now carry roofs in the 15-to-25-year range, and admitted carriers have drawn hard lines.

Most admitted carriers in Florida will not write a new policy on a home with a roof older than 15 years without either requiring replacement within a defined period or excluding roof damage from coverage. Some won’t quote at all. The threshold varies by carrier; some cut off earlier for certain roof types.

Gable roofs — the classic triangular design common in Orlando subdivisions built through the 1990s — are structurally more vulnerable in wind events than hip roofs, where all four sides slope down to the walls. Carriers price that difference explicitly. A home in 32825 with a 15-year-old gable roof is a harder placement than the same home with a hip roof, and the combination of age and shape often disqualifies a property from the mainstream admitted market entirely.

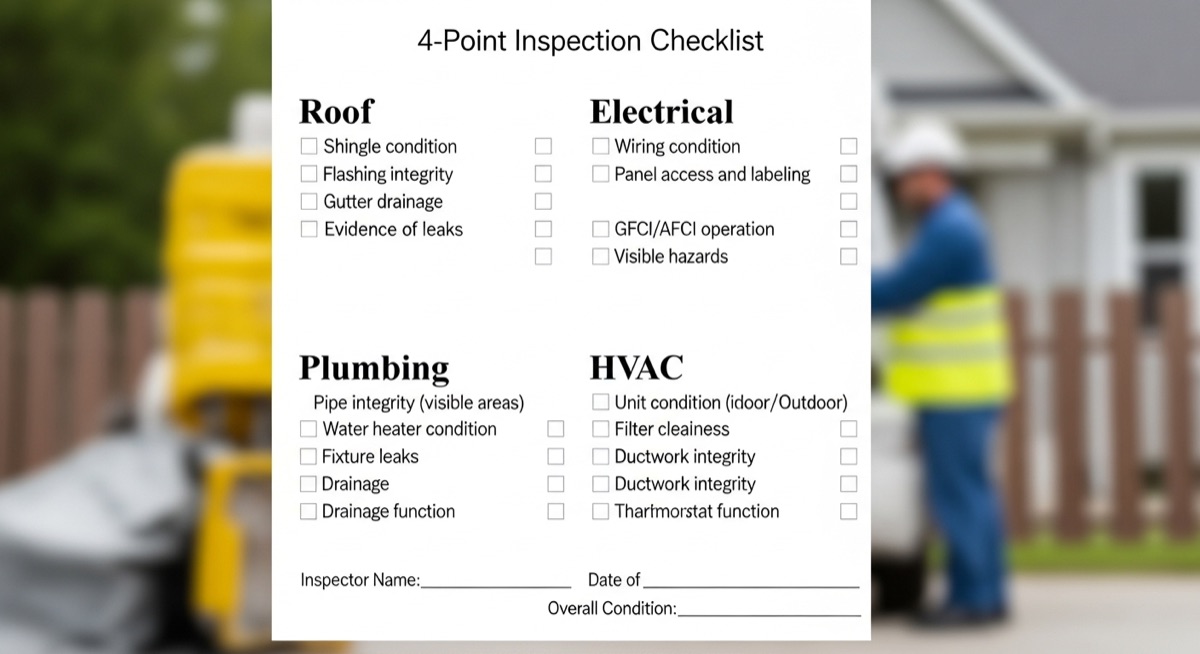

Most carriers asking about roof age want one or both of two inspections: a 4-point inspection (covering roof, electrical, plumbing, and HVAC) and a separate wind mitigation inspection. The 4-point is required by most admitted carriers for homes over 10 years old. It’s an eligibility gate, not a credit calculator. The wind mitigation inspection generates the credits that actually reduce your premium. As part of our home & property coverage, we’ve tracked how these inspection requirements are reshaping the buying and selling calculus across Central Florida’s aging housing stock.

Here’s the divide reshaping the market in practical terms: a homeowner in 32825 with a 17-year-old gable roof faces completely different underwriting than a buyer in Lake Nona (32832) whose home was built in 2018. Hip roof, still within most carriers’ favorable credits window, qualifies for wind mitigation discounts, draws no age surcharge. The underwriting world is, for all purposes, two separate markets right now. New construction in Lake Nona, Horizon West (34787), and Laureate Park — built under the post-2010 Florida Building Code — qualifies for wind mitigation treatment that older Central Florida housing stock simply cannot access.

Wind Mitigation Inspections — What They Cost, What They Actually Save

The advice to “get a wind mitigation inspection” is common enough to have become background noise. Here’s what it actually involves and what it’s worth for Central Florida construction — because the range is wide enough that it matters which side of it your house lands on.

A wind mitigation inspection evaluates specific structural features that affect how your home performs in high-wind events. A licensed inspector documents your roof covering type, roof deck attachment, roof-to-wall connection type, roof shape (hip vs. non-hip), secondary water resistance (a membrane layer between the deck and shingles that prevents water intrusion if shingles are lost), and opening protections (hurricane shutters or impact-resistant windows and doors).

The inspection takes about 45 minutes to an hour on-site and costs $75 to $150 from most licensed inspectors in the Orlando area. The resulting standardized wind mitigation report is what you submit to your insurer. Carriers are required to apply credits to the wind portion of your premium for each favorable feature documented. Credits can reduce the wind portion of your premium by 10 to 45 percent under Florida’s wind mitigation credit schedule.

For concrete block construction with a hip roof, secondary water resistance, and hurricane shutters — common in newer Dr. Phillips and Lake Nona developments — credits can approach the upper end of that range. A $100 inspection that saves $800 a year is worth doing before lunch.

For gable-roof concrete block construction without shutters — the dominant profile in older East Orlando subdivisions — credits are more modest. Roof-to-wall connections documented as clips or wraps rather than toe nails still generate savings, and secondary water resistance, if present, merits crediting. But without a hip roof and without opening protections, significant credit categories stay empty.

The three features that produce the largest credits under Florida’s schedule: hip roof shape, secondary water resistance, and opening protections rated to current Florida Building Code standards. If you’re doing a reroof and have any flexibility in the budget, ask your roofing contractor about installing secondary water resistance during the reroof. The cost is modest. The annual credit is ongoing. It’s one of the more straightforward insurance decisions you can make in this market. For a broader look at high-impact home improvements ranked by dollar savings, our earlier analysis shows where insurance upgrades stack up against energy and maintenance spending.

The Coverage Gap Nobody Talks About — Sinkhole Risk in Orange County

Florida’s sinkhole risk is concentrated in the I-4 corridor — the Tampa-to-Daytona band that runs directly through Orange County. Orange County sits on the southern edge of what geologists call Florida’s “sinkhole alley,” with documented activity concentrated in the northwest quadrant: ZIP codes 32818 and 32808, and parts of 32825.

Florida law requires all admitted homeowner carriers to include catastrophic ground cover collapse (CGCC) coverage by default. CGCC covers the dramatic, sudden scenario: ground collapses, structure drops, you call 911. What it does not cover is the slower, more common manifestation of sinkhole activity — gradual subsidence, stair-step cracking in block walls, doors that no longer close properly — which requires full sinkhole coverage, a separately priced endorsement that many carriers no longer offer and that others price at levels that make it inaccessible for budget-constrained homeowners.

The distinction matters most in northwest Orange County, where the underlying karst geology creates ongoing risk of slow subsidence that won’t meet CGCC’s threshold (sudden, visible, verifiable) but can cause serious structural damage over months or years. It’s the kind of damage that looks like a settling house right up until a structural engineer tells you it isn’t.

Homeowners in 32818 and 32808 who haven’t specifically asked about and added sinkhole coverage may lack protection for damage that a structural engineer would attribute to subsidence. When shopping in these ZIP codes, ask your agent explicitly: does this carrier offer full sinkhole coverage, and what does it cost? Some carriers won’t offer it in these ZIP codes at all; others will offer it with a separate, substantial deductible. Surplus lines may be your only option if you want both a competitive rate and sinkhole coverage in the most active areas. No online insurance comparison tool is going to flag this for you. This is one of the calls where a local agent who knows the county actually earns their commission.

Condo and HOA Owners — Your Insurance Problem Is Different

Orlando has a large and growing condo and HOA housing stock, particularly in downtown (32801), Dr. Phillips (32836), Baldwin Park (32814), Lake Nona (32832), and Celebration (34747 in Osceola County). The insurance question for unit owners in these communities is structurally different from what faces single-family homeowners, and it’s the most consistently misunderstood coverage situation in the region.

An HOA’s master policy covers the building structure, common areas, and — depending on how the master policy is written — some or all of the original interior fixtures of your unit. It does not cover your personal property, improvements and betterments you’ve made (upgraded flooring, custom cabinetry, kitchen renovations), additional living expenses if you’re displaced, or your personal liability. An HO-6 policy addresses that gap.

The critical variable is where the building coverage stops and your personal exposure begins. Most Central Florida HOA communities use some variant of a structure-only or modified structure approach, which means unit owners who haven’t reviewed their master policy declarations may be significantly underinsured for interior finishes.

One downtown condo owner discovered after a kitchen fire that her master policy covered only “builder-grade” finishes, and her remodeled kitchen fell outside that definition, creating a $40,000 gap that her personal HO-6 policy didn’t cover because the fire originated in a common area. That’s not a legal technicality. That’s $40,000 she had to find somewhere.

Citizens depopulation also plays out differently in the condo market. Unit owners should pay particular attention to whether an assuming carrier is willing to underwrite the specific building’s characteristics — age of electrical systems, roof condition on low-rise buildings — not just the ZIP code. Some carriers that write single-family homes won’t take condominium business in certain buildings because the building’s maintenance profile disqualifies it from their underwriting appetite.

For buyers entering the condo market in Celebration or Lake Nona, the HOA’s master policy is a document you should read before closing. Your real estate attorney or insurance agent can review the declarations and identify where your personal coverage needs to begin. Coverage gaps in condo communities are producing claims disputes that are costly and slow to resolve, and they’re almost entirely avoidable with upfront review.

How to Shop This Market — Independent Agents, Surplus Lines, and What to Avoid

For most Orange County homeowners shopping in 2026, an independent agent with access to multiple Florida-domestic carriers is more useful than a captive agent representing a single company. The national carriers that dominated this market historically aren’t writing new business here. An independent agent with appointments at Universal, HCI, Security First, Slide, Tower Hill, and a surplus lines broker can survey what’s actually available for your specific property. That breadth of access is the whole point.

When no admitted carrier will write your home — or when the only admitted option has conditions you can’t meet — surplus lines carriers are the backstop. Lloyd’s of London syndicates and other non-admitted carriers operating through licensed surplus lines brokers can write risks that the standard market won’t touch. Policy terms can vary considerably from the standardized forms admitted carriers use, and consumer protections differ. Surplus lines is often the right answer for specific situations: pre-1985 construction, active sinkhole areas, properties in flood zones. But go in clear-eyed. You’re not getting a worse product, necessarily — you’re getting a different one, with different rules.

A few things worth checking before you bind any policy in the current market:

Verify Demotech ratings at the time of binding, not when the agent quoted you. Ratings can and do change. A downgrade after you bind can trigger a force-placed insurance requirement from your lender — typically a far more expensive, far less comprehensive policy. Force-placed insurance is one of those things that sounds manageable until you see the premium.

Read your wind deductible carefully. Most Florida policies use a percentage deductible for wind rather than a flat dollar amount. On a $350,000 home, a 2 percent wind deductible means you pay the first $7,000 of any wind claim out of pocket. The declarations page lists it explicitly; compare it across the quotes you receive, not just the annual premium.

If you live in an HOA community, get the master policy declarations and read them before you buy your HO-6. What the master policy covers determines how much dwelling coverage your personal policy needs to carry.

Finally, if you’re working with an agent you haven’t used before, verify their license through the Florida Department of Financial Services’ license verification tool. It takes thirty seconds. No exceptions.

CityDesk Orlando will update this report as Citizens announces additional depopulation rounds and as FLOIR approves rate filings affecting Orange, Seminole, and Osceola counties. Readers with premium quotes or non-renewal experiences to share can reach us at the contact link below.